RedStickBR

| Favorite team: | LSU |

| Location: | |

| Biography: | |

| Interests: | |

| Occupation: | |

| Number of Posts: | 14577 |

| Registered on: | 9/29/2009 |

| Online Status: | Not Online |

Recent Posts

Message

re: Discussion of Fed Liquidity’s Impact on Equity Markets

Posted by RedStickBR on 10/21/21 at 9:34 am to wutangfinancial

quote:

Treasury auction today says if you come at the king you best not miss. PM participation even lower according to Santeli than the past several auctions. But remember we're printing money. German bunds got bid and they hit their highest inflation marks in quite some time. Just another big market to keep an eye on. German recession tipped off the global trade contraction for me in 2019, and that's when everything began to break.

That is very interesting. I haven't been nerding out on the Treasury auctions results like I should be. I imagine Wolf Richter has some insights on this. Will post anything I find, and good catch.

1

1

re: Private Equity investment. Anyone used PE to generate alpha?

Posted by RedStickBR on 10/9/21 at 1:22 am to buckeye_vol

PE is another victim of low rates. As investors search for yield in a low yield world, they go further and further out the risk curve. Generally speaking, the lower the risk of an investment, the larger the market, such that the bond market > the equity market > the PE market > the VC market.

As more capital is allocated to riskier investments, the pig moves through the python, deal competition increases, and yields get compressed. In my experience, it’s hard to find alpha unless you’re in a market that is too small to attract much interest from institutional players (which is why I struggle with why ordinary people want to do things like get into the storage unit business after that industry has already been flooded with REIT money).

There are no doubt PE firms out there who generate alpha based on their industry expertise or because they’ve carved out a niche. But those managers are few and far between, and the better they do, the more inaccessible they become for smaller investors.

LINK

As more capital is allocated to riskier investments, the pig moves through the python, deal competition increases, and yields get compressed. In my experience, it’s hard to find alpha unless you’re in a market that is too small to attract much interest from institutional players (which is why I struggle with why ordinary people want to do things like get into the storage unit business after that industry has already been flooded with REIT money).

There are no doubt PE firms out there who generate alpha based on their industry expertise or because they’ve carved out a niche. But those managers are few and far between, and the better they do, the more inaccessible they become for smaller investors.

LINK

re: Discussion of Fed Liquidity’s Impact on Equity Markets

Posted by RedStickBR on 9/30/21 at 7:24 am to wutangfinancial

I’m sure you’ve noticed King Dollar throwing its weight around here recently …

re: Discussion of Fed Liquidity’s Impact on Equity Markets

Posted by RedStickBR on 9/28/21 at 11:57 am to wutangfinancial

Any uptick at all today?

And that chart may go down as the poster child of distortions in financial markets. :lol:

And that chart may go down as the poster child of distortions in financial markets. :lol:

re: It’s Fed day; put your predictions here.

Posted by RedStickBR on 9/28/21 at 10:07 am to Chucktown_Badger

I don’t find it coincidental that the $3.5T build back better plan is talking about being trimmed back on the same day that Powell admitted inflation is hotter than expected and yields are blowing out.

If 10y goes back towards 1.7%, might be a good Treasury buying opportunity on a bet the fiscal gets pared back due to inflation concerns.

If 10y goes back towards 1.7%, might be a good Treasury buying opportunity on a bet the fiscal gets pared back due to inflation concerns.

re: Discussion of Fed Liquidity’s Impact on Equity Markets

Posted by RedStickBR on 9/28/21 at 9:59 am to wutangfinancial

Today’s macro heat map is doing what you would expect to see if everyone went risk-off. Not saying that’s happening, just noting the pattern:

1. Nasdaq down more than S&P down more than DJIA

2. Yields up

3. Dollar up

That, to me, is the quintessential risk-off combo. Did I miss any?

1. Nasdaq down more than S&P down more than DJIA

2. Yields up

3. Dollar up

That, to me, is the quintessential risk-off combo. Did I miss any?

re: Discussion of Fed Liquidity’s Impact on Equity Markets

Posted by RedStickBR on 9/25/21 at 12:10 pm to Turf Taint

Sure, so when the original post was made, there was a lot of commentary out there that the “Fed’s QE was making its way into the market.” The original purpose of the thread was to (a) determine whether or not that could actually be proven to be true and (b) if so, how one could “follow the money,” so to speak.

Over the course of the thread we’ve learned a lot about what QE is and what it’s not. At a basic level, we determined that it’s little more than an asset swap. The Fed creates digital reserves and uses those to buy Treasuries from banks, in the process reducing the average duration of the liability side of its balance sheet (i.e. all of those newly issued reserves are essentially over night cash liabilities to the Fed). Moreover, the Fed’s purchases of Treasuries creates additional demand for Treasuries and in a manner that is very price agnostic. As such, that can tend to put upward pressure on Treasury prices and downward pressure on Treasury rates relative to where those rates would be required to be if private market participants were the only ones doing all the purchasing.

In understanding that, I think I can say the board has collectively realized that the Fed’s QE isn’t necessarily “finding its way into the markets,” but rather has a more indirect impact on markets in that the additional demand for Treasuries puts downward pressure on Treasury rates which in turn puts downward pressure on equity yields (upward pressure on equity prices), assuming equity yields maintain a constant spread against Treasury yields. The other factor that has become apparent is that the Fed’s dovish messaging, giving market participants the impression that “the Fed has their backs,” causes risk to be priced with a much lower premium that what you’d expect relative to historical volatility and current valuation.

So, QE is putting downward pressure on bond yields (and by extension, equity yields) and its “whatever it takes” mentality is causing market participants to exert further downward pressure on equity yields in the form of a shrinking equity risk premium relative to history (which, in a perfect world, would be the opposite of what you’d expect to see in an environment of very high valuations; high valuations should mean lower expected returns which in turn should mean lower tolerance for risk).

We’ve also talked a lot about whether or not QE is inherently inflationary. The conclusion I’ve come to is that it’s not inherently inflationary, and could even be deflationary in that artificially low rates cause capital to be allocated towards projects that are increasingly unattractive, with said inefficient use of capital having a drag on productivity, and with said drag on productivity having a stagnating or deflationary effect on the economy at large.

Nonetheless, given that QE creates bank reserves, and bank reserves can be leveraged by banks to increase loans, QE can be inflationary if instead of sitting idle on bank balance sheets those reserves result in a greater quantity of money in the real economy. We’ve noticed many banks are still being somewhat conservative with their lending given low net interest margins and fewer opportunities for attractive risk-adjusted loans. So, QE can be thought of as planting the seeds for potential inflation, but whether those seeds grow into inflation-bearing trees is in large part dependent upon what banks do with them (hoard them or loan against them).

That said, there has been one aspect with this current QE that has been different than previous versions, and that’s that recent QE has been implemented with a view towards not just buying Treasuries from private markets but enabling government deficit spending, and much of that spending (stimulus payments, etc.) has been in the form of helicopter money directly to lower and middle income people who are more likely to spend it. That has been a form of inflationary pressure (M2 expansion) that wasn’t as prevalent in previous QEs.

What to make of all of this? The Fed’s actions can have indirect and quasi-direct impacts on markets primarily through the mechanisms of relative asset class yields and investor perceptions towards risk. To date, we haven’t seen the direct impact some other countries have, wherein central banks actually start buying equities themselves. The Fed’s actions can also have indirect, quasi-direct or even direct (if you’re a monetarist) impacts on inflation, particularly if it enables fiscal spending into segments of society most likely to spend those dollars back into the economy. But it can also be long-term deflationary if it causes things like capital to be misallocated, zombie companies to “remain on the shelf” beyond their expiration date, and governments, businesses and households to take on too much debt which eventually requires belt-tightening in order to repay.

There you have it. I know it’s a lot, but the thread has covered a lot. There are surely others like wutang and Cork who may have more to add or who may disagree with or see things differently than what I’ve described above. :cheers:

Over the course of the thread we’ve learned a lot about what QE is and what it’s not. At a basic level, we determined that it’s little more than an asset swap. The Fed creates digital reserves and uses those to buy Treasuries from banks, in the process reducing the average duration of the liability side of its balance sheet (i.e. all of those newly issued reserves are essentially over night cash liabilities to the Fed). Moreover, the Fed’s purchases of Treasuries creates additional demand for Treasuries and in a manner that is very price agnostic. As such, that can tend to put upward pressure on Treasury prices and downward pressure on Treasury rates relative to where those rates would be required to be if private market participants were the only ones doing all the purchasing.

In understanding that, I think I can say the board has collectively realized that the Fed’s QE isn’t necessarily “finding its way into the markets,” but rather has a more indirect impact on markets in that the additional demand for Treasuries puts downward pressure on Treasury rates which in turn puts downward pressure on equity yields (upward pressure on equity prices), assuming equity yields maintain a constant spread against Treasury yields. The other factor that has become apparent is that the Fed’s dovish messaging, giving market participants the impression that “the Fed has their backs,” causes risk to be priced with a much lower premium that what you’d expect relative to historical volatility and current valuation.

So, QE is putting downward pressure on bond yields (and by extension, equity yields) and its “whatever it takes” mentality is causing market participants to exert further downward pressure on equity yields in the form of a shrinking equity risk premium relative to history (which, in a perfect world, would be the opposite of what you’d expect to see in an environment of very high valuations; high valuations should mean lower expected returns which in turn should mean lower tolerance for risk).

We’ve also talked a lot about whether or not QE is inherently inflationary. The conclusion I’ve come to is that it’s not inherently inflationary, and could even be deflationary in that artificially low rates cause capital to be allocated towards projects that are increasingly unattractive, with said inefficient use of capital having a drag on productivity, and with said drag on productivity having a stagnating or deflationary effect on the economy at large.

Nonetheless, given that QE creates bank reserves, and bank reserves can be leveraged by banks to increase loans, QE can be inflationary if instead of sitting idle on bank balance sheets those reserves result in a greater quantity of money in the real economy. We’ve noticed many banks are still being somewhat conservative with their lending given low net interest margins and fewer opportunities for attractive risk-adjusted loans. So, QE can be thought of as planting the seeds for potential inflation, but whether those seeds grow into inflation-bearing trees is in large part dependent upon what banks do with them (hoard them or loan against them).

That said, there has been one aspect with this current QE that has been different than previous versions, and that’s that recent QE has been implemented with a view towards not just buying Treasuries from private markets but enabling government deficit spending, and much of that spending (stimulus payments, etc.) has been in the form of helicopter money directly to lower and middle income people who are more likely to spend it. That has been a form of inflationary pressure (M2 expansion) that wasn’t as prevalent in previous QEs.

What to make of all of this? The Fed’s actions can have indirect and quasi-direct impacts on markets primarily through the mechanisms of relative asset class yields and investor perceptions towards risk. To date, we haven’t seen the direct impact some other countries have, wherein central banks actually start buying equities themselves. The Fed’s actions can also have indirect, quasi-direct or even direct (if you’re a monetarist) impacts on inflation, particularly if it enables fiscal spending into segments of society most likely to spend those dollars back into the economy. But it can also be long-term deflationary if it causes things like capital to be misallocated, zombie companies to “remain on the shelf” beyond their expiration date, and governments, businesses and households to take on too much debt which eventually requires belt-tightening in order to repay.

There you have it. I know it’s a lot, but the thread has covered a lot. There are surely others like wutang and Cork who may have more to add or who may disagree with or see things differently than what I’ve described above. :cheers:

re: Discussion of Fed Liquidity’s Impact on Equity Markets

Posted by RedStickBR on 9/24/21 at 8:16 pm to wutangfinancial

So the Fed basically started selling Treasuries to get rates back up to a point that other people wanted to buy them?

re: Discussion of Fed Liquidity’s Impact on Equity Markets

Posted by RedStickBR on 9/22/21 at 1:45 pm to wutangfinancial

I had to turn away for a minute, but do I have it right that he started off super dovish with no mention of taper in his prepared remarks and then snuck in “taper could be ended by middle of next year” and “could begin next month” in response to these last few questions?

re: Current Market

Posted by RedStickBR on 9/20/21 at 3:04 pm to rocket31

:lol: That’s just blatantly false. I’ve said I think they should raise rates. I’ve said I think inflation or the market could or should cause them to raise rates. I’ve noted there were members of the FOMC who appeared to be becoming more open to raising rates sooner rather than later. But in no way have I been making “eights months in a row of predictions of imminent Fed rate hikes.”

It’s only a matter of time before your binary view of the world causes significant damage to your portfolio. You have an almost religious conviction of your finance and economic views. The definition of “Bayesian” could be “doing something in the manner that is the exact opposite of rocket31.” Get out of here with your nonsense.

It’s only a matter of time before your binary view of the world causes significant damage to your portfolio. You have an almost religious conviction of your finance and economic views. The definition of “Bayesian” could be “doing something in the manner that is the exact opposite of rocket31.” Get out of here with your nonsense.

re: Current Market

Posted by RedStickBR on 9/20/21 at 2:29 pm to CorkRockingham

quote:

For the health and well being of future generation I wish this market would correct and that that the Fed would taper and that they would raise interest rates.

+1

re: Current Market

Posted by RedStickBR on 9/20/21 at 1:50 pm to FLObserver

Retail investors have been so convinced of “buy the dip,” “there is no alternative,” “stonks only go up,” and “don’t fight the Fed,” that there is no way they get out in time. If the market tanks, they will go down with it. That said, there are at least some trading signals that may pique their interest. For instance, the S&P’s RSI hasn’t been this low since March of 2020 and we certainly don’t appear to be bouncing off the 50-day moving average like we have half a dozen times or so in the past few months. So maybe they do get tempted to get a little cautious here.

Kyle Bass had some interesting comments recently with Grant Williams where he mentioned it has become a known fact in macro circles that Fed officials enjoy seeing how the market reacts to their comments (dual mandate, right?). I wouldn’t be surprised if we get a Fed bounce this week, even with my view that current valuations are firmly divorced from reality.

Kyle Bass had some interesting comments recently with Grant Williams where he mentioned it has become a known fact in macro circles that Fed officials enjoy seeing how the market reacts to their comments (dual mandate, right?). I wouldn’t be surprised if we get a Fed bounce this week, even with my view that current valuations are firmly divorced from reality.

re: Futures look like crap

Posted by RedStickBR on 9/20/21 at 8:16 am to wutangfinancial

:lol: When our banks get in trouble, we bail them out or call them too big to fail. Is CCP giving the world a lesson in capitalism, or will they end up doing the same thing we do?

re: Dedicated Short / Put Thread

Posted by RedStickBR on 9/16/21 at 8:44 pm to Jag_Warrior

GSKY announced it was to be acquired by Goldman, so that hasn’t helped. Overall, though, still up triple digits on the strategy as a whole. It’s become more difficult recently, which might seem counterintuitive, but if you look at a chart of the Russell 2000, small caps haven’t sold off as much as you’d think. Going to keep it going though, because if and when we have a shite the bed moment, that’s when the returns will go parabolic.

re: Fed hides weekly M1 supply, says "money doesn't matter"

Posted by RedStickBR on 9/15/21 at 10:51 am to wutangfinancial

I haven’t seen that yet, but I don’t doubt it. Can you imagine if they overcooked this thing so much so that Real GDP is negative this year? :lol:

Also a good read:

LINK

Also a good read:

LINK

re: Fed hides weekly M1 supply, says "money doesn't matter"

Posted by RedStickBR on 9/14/21 at 8:26 pm to wutangfinancial

re: Putting the massive fiscal into perspective

Posted by RedStickBR on 9/10/21 at 11:47 am to LSUFanHouston

I’m not referring to paying it off entirely. Of course we shouldn’t do that. I could have been clearer on that point.

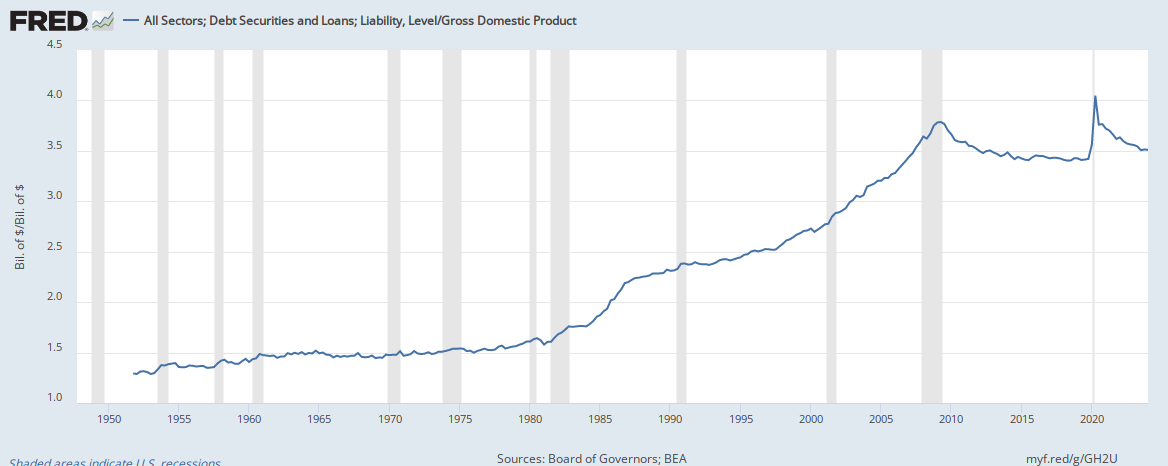

I’m referring to even getting Debt to GDP down to a meaningful level short of financial repression, Fed monetizing the debt and then effectively writing it off, defaults and restructurings, or some sort of economic growth miracle.

Even the MMTers recognize inflation as a constraint on deficit spending. Absent financial repression, how will we ever get back to, say, pre-COVID debt to GDP levels? Or do we not need to because interest rates are low? In which case, are we admitting the Fed will never be able to raise rates again? Because refinancing this at higher rates will be a bitch:

I’m referring to even getting Debt to GDP down to a meaningful level short of financial repression, Fed monetizing the debt and then effectively writing it off, defaults and restructurings, or some sort of economic growth miracle.

Even the MMTers recognize inflation as a constraint on deficit spending. Absent financial repression, how will we ever get back to, say, pre-COVID debt to GDP levels? Or do we not need to because interest rates are low? In which case, are we admitting the Fed will never be able to raise rates again? Because refinancing this at higher rates will be a bitch:

re: Putting the massive fiscal into perspective

Posted by RedStickBR on 9/10/21 at 8:52 am to wutangfinancial

That PPI report :lol: And we are basically beyond the y/y base effect comps at this point, yet Core y/y PPI just accelerated by 260bps compared to the first base effect month (May report for Apr month).

That fiscal and monetary and unemployment benefit and eviction moratorium cliff we are about to see should go overly splendidly in a 350%+ Debt to GDP economy.

That fiscal and monetary and unemployment benefit and eviction moratorium cliff we are about to see should go overly splendidly in a 350%+ Debt to GDP economy.

Putting the massive fiscal into perspective

Posted by RedStickBR on 9/9/21 at 10:12 pm

I came across this statistic today and it really got the macro wheels turning in terms of understanding just how large the trillions in US stimulus is.

The electricity industry is the most capital intensive industry on the planet, with global capex of $780 billion. Oil and gas is second, with global capex of $760 billion. (source: A Question of Power, by Robert Bryce).

The 2020 US deficit alone (which is just the deficit, not total spending) was $3.1 trillion. Thus, the US deficit spending alone (again, not total spending) was akin to all capex for the electricity industry AND the oil and gas industry across the ENTIRE world, times TWO.

And yet we are just now back to sniffing out the pre-COVID trend line in terms of nominal GDP (in real terms, it’s even worse), even though in 2020 we spent enough money to maintain the equivalent of multiple global electric grids and oil and gas complexes …

We will never pay off the debt.

The electricity industry is the most capital intensive industry on the planet, with global capex of $780 billion. Oil and gas is second, with global capex of $760 billion. (source: A Question of Power, by Robert Bryce).

The 2020 US deficit alone (which is just the deficit, not total spending) was $3.1 trillion. Thus, the US deficit spending alone (again, not total spending) was akin to all capex for the electricity industry AND the oil and gas industry across the ENTIRE world, times TWO.

And yet we are just now back to sniffing out the pre-COVID trend line in terms of nominal GDP (in real terms, it’s even worse), even though in 2020 we spent enough money to maintain the equivalent of multiple global electric grids and oil and gas complexes …

We will never pay off the debt.

re: Dedicated Short / Put Thread

Posted by RedStickBR on 8/26/21 at 10:47 pm to Jag_Warrior

Thanks :cheers:

I’ve intentionally tried to time stamp all my entries and exits. The strategy had a perfect track record up until JYNT, and I’m currently slightly in the red on a combined basis for the last three I posted about. But I’m hopeful that my macro view and the Russell 2000 flatlining mean the strategy will have a massive payoff if we see another big correction in the S&P.

I’ve intentionally tried to time stamp all my entries and exits. The strategy had a perfect track record up until JYNT, and I’m currently slightly in the red on a combined basis for the last three I posted about. But I’m hopeful that my macro view and the Russell 2000 flatlining mean the strategy will have a massive payoff if we see another big correction in the S&P.

re: Dedicated Short / Put Thread

Posted by RedStickBR on 8/26/21 at 10:44 pm to CorkRockingham

I mean ITM from a put perspective. So if a speculative small cap goes from 4 to 9 quickly and then begins to rollover, I wager that retail’s short attention span will cause them to unload and move on to the next thing. In that scenario, I may buy a put with a 10 strike.

Popular