RoyalWe

| Favorite team: | LSU |

| Location: | Louisiana |

| Biography: | |

| Interests: | LSU Basketball / Football |

| Occupation: | Retired Engineer |

| Number of Posts: | 5241 |

| Registered on: | 3/15/2018 |

| Online Status: | Not Online |

Recent Posts

Message

re: Update pg 3 - 43" bar information home assistant display now in beta!

Posted by RoyalWe on 7/21/26 at 12:37 pm to AaronDeTiger

Just a note to say you guys are killing me with everything you're doing. I'm going to re-read this entire thread to understand how I can get up to speed so I can get in the game. I'm having a ball messing around with the ESP32, but just installed Home Assistant and Uptime Kuma to expand what I report. Having said that, I want a big arse screen with nice graphics. I'm willing to invest in some automation devices as well.

Well done, guys.

Well done, guys.

1

1

re: Is this generation of young people the most different of any generation ever?

Posted by RoyalWe on 7/20/26 at 5:25 pm to slidingstop

My buddy, El Gaucho, will be along shortly to put you in your place.

quote:I'll look into this. Right now I'm using "packages" on the HA side that create JSON when called by the ESP32. It's working well, though. I've got thermostat-related data from my Ecobees and Synology NAS status information. It worked without a hitch. I'm really impressed with the entire workflow/process and I can easily see myself buying a large touchscreen and developing something either for HA or ESP32 -- or both. I'm sure this is going to encourage me to buy more home automation stuff. This retired nerd is in trouble.

The ESP32 supports MQTT

I've been careful about keeping any tokens or keys out of code in Google Apps Script and Arduino IDE's C code. I've segregated and excluded any files from Git scrutiny and just keep example files of sensitive stuff so others could follow. No doubt what you're suggesting would be a wild ride, but I need to learn more about it and see what boundaries I might enforce. I've been really pleased just directing ChatGPT with what I want done and learning the work flow that I'm happy to keep doing that. Maybe once I get comfortable with Cline or other CLIs I'll try something.

re: I Tried to Build a C64-themed Clock and Failed

Posted by RoyalWe on 7/19/26 at 3:51 pm to LemmyLives

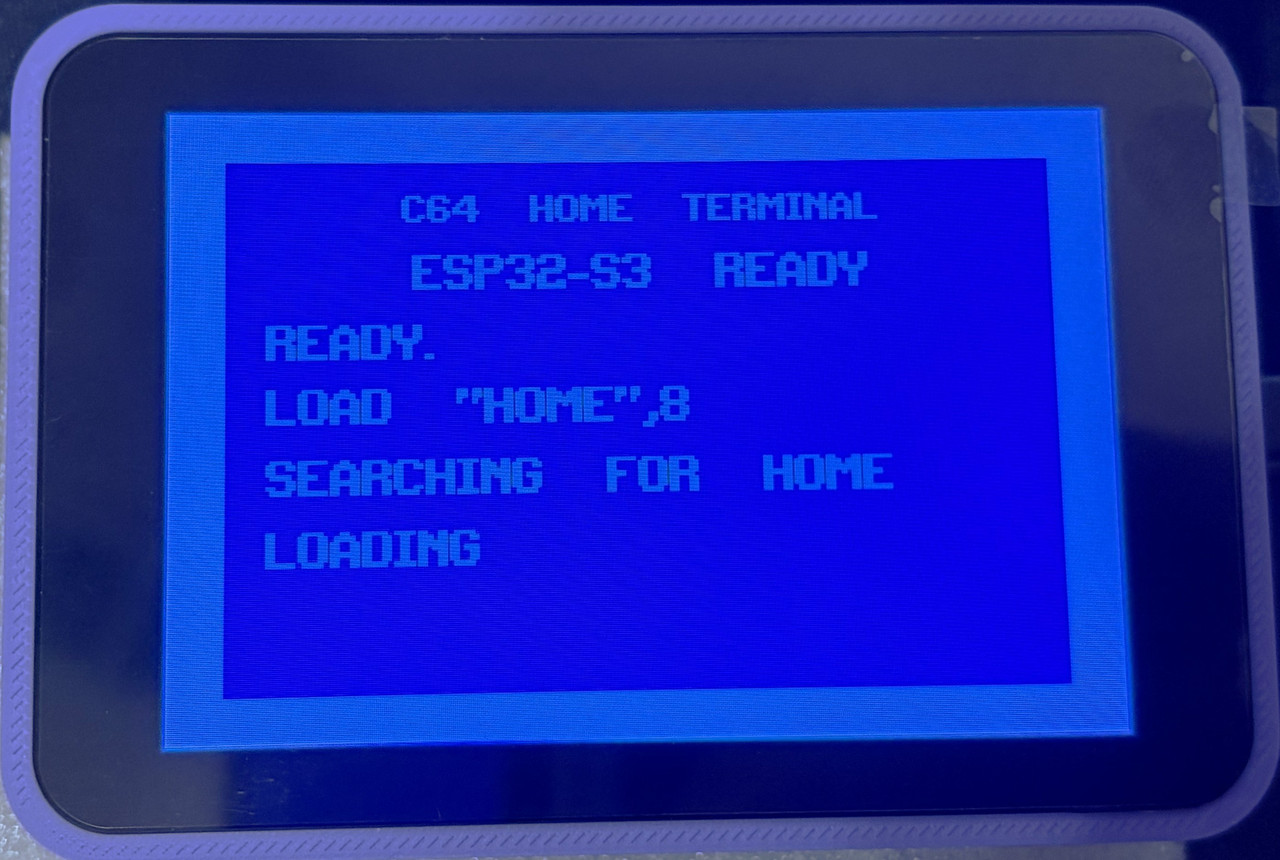

Here are a few shots. I 3D printed a case for it, but will probably make a Commodore 64 version at some point. I plan on having a more modern theme on a larger board eventually. Unfortunately I had to take actual photos of the screens because the method I use won't allow for it, but that will change.

This boot sequence is a head nod to Commodore 64 loading a program.

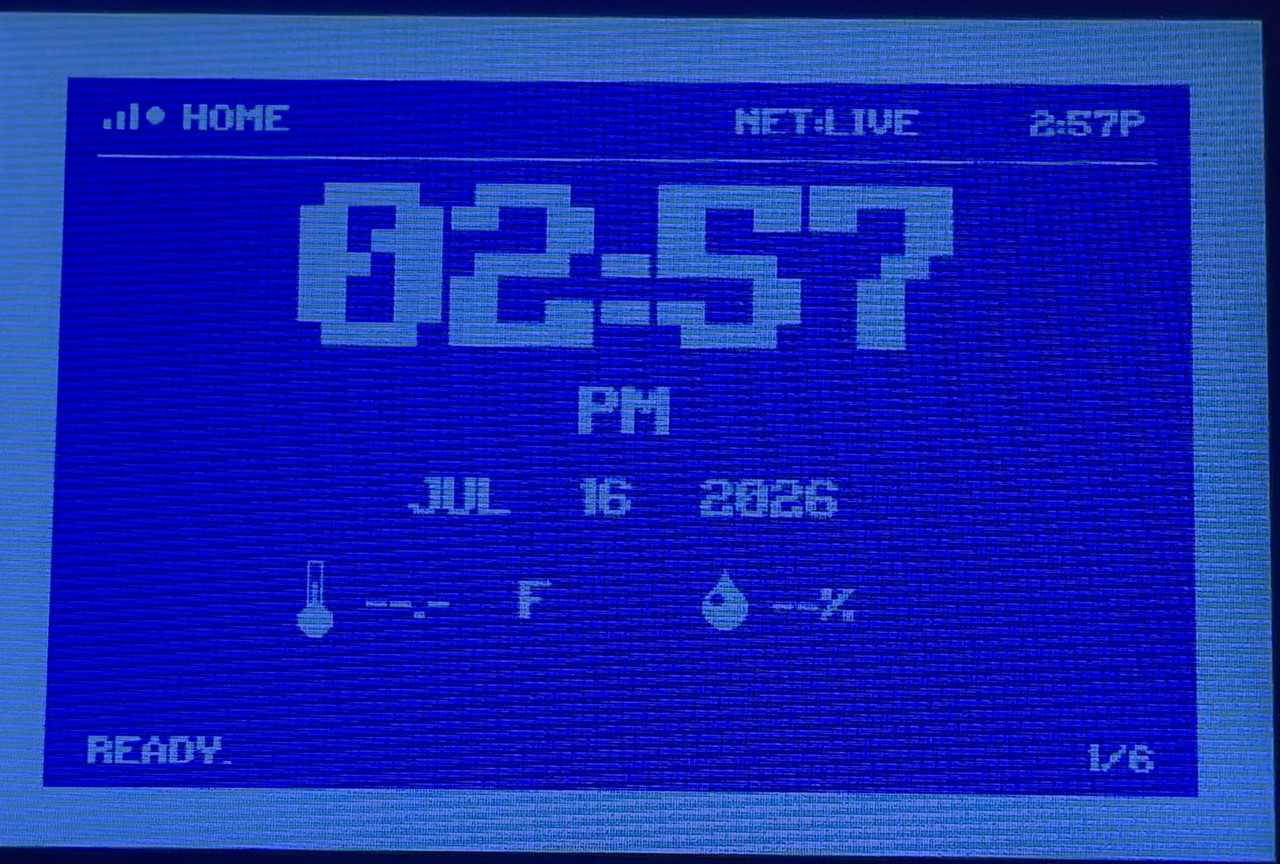

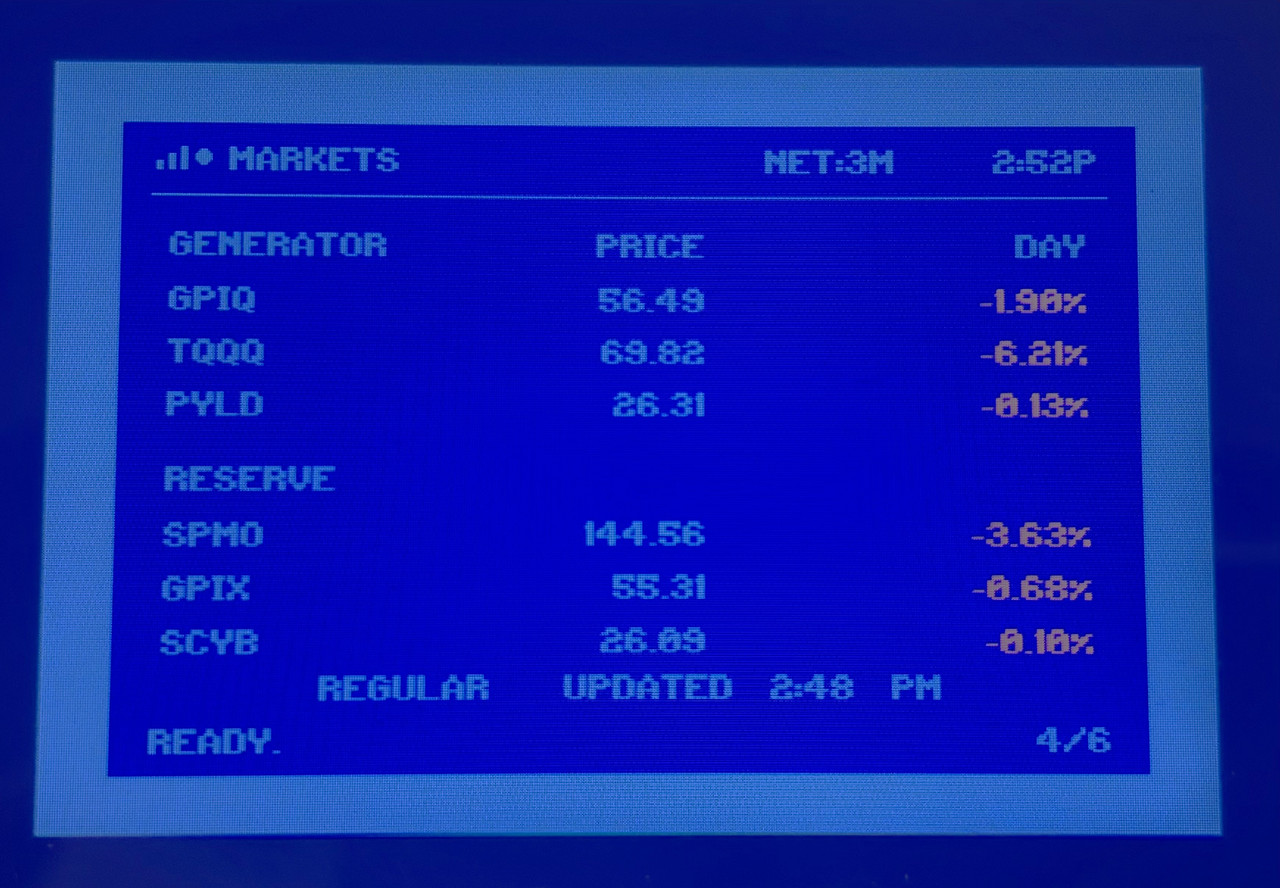

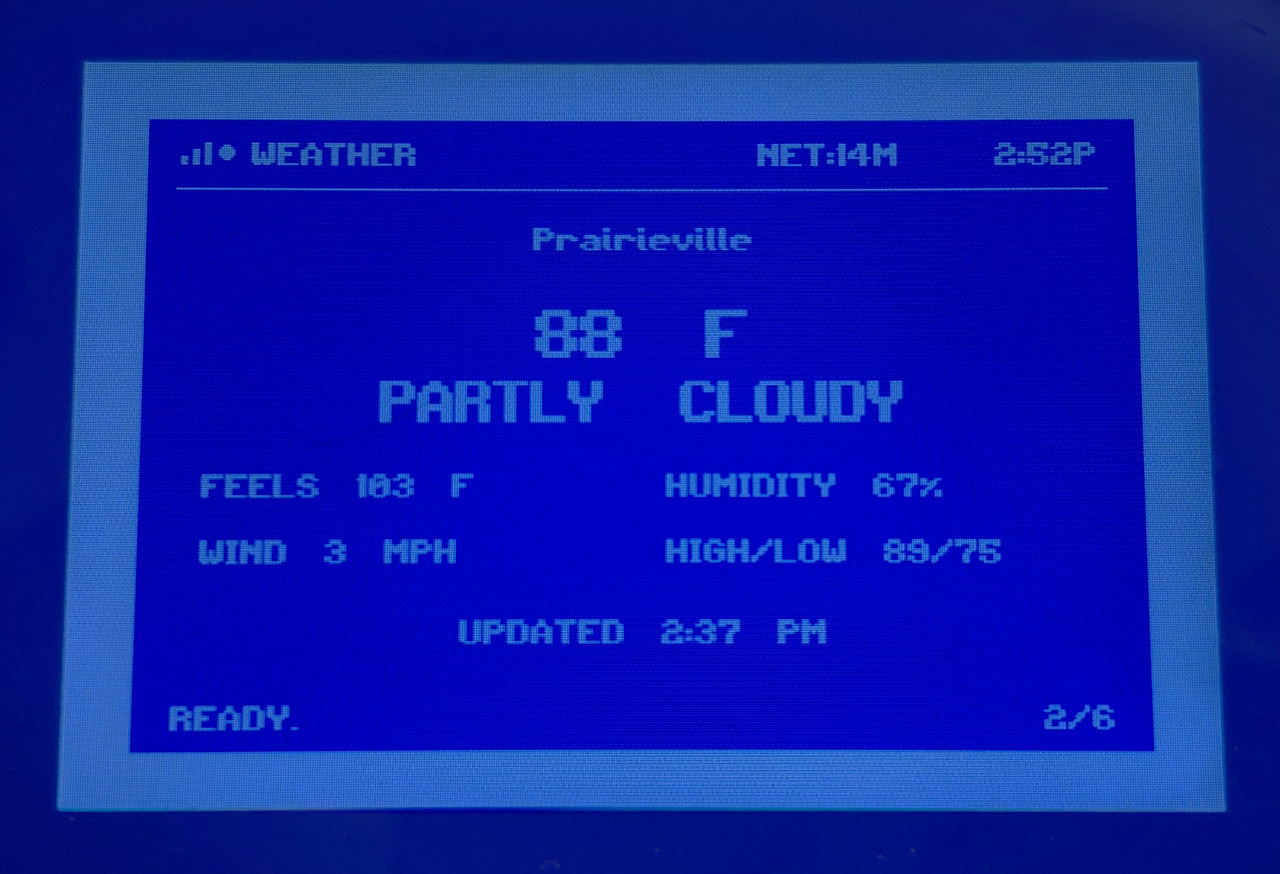

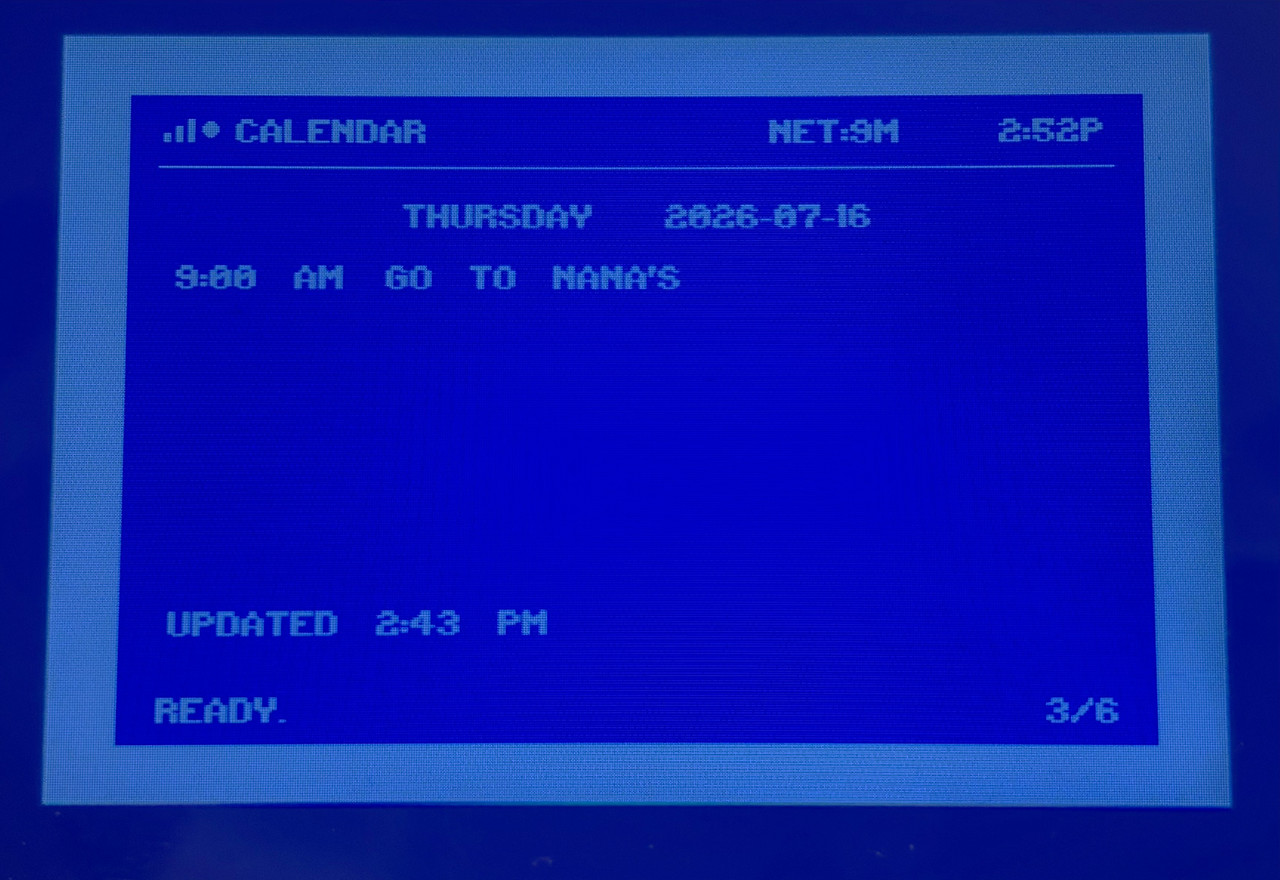

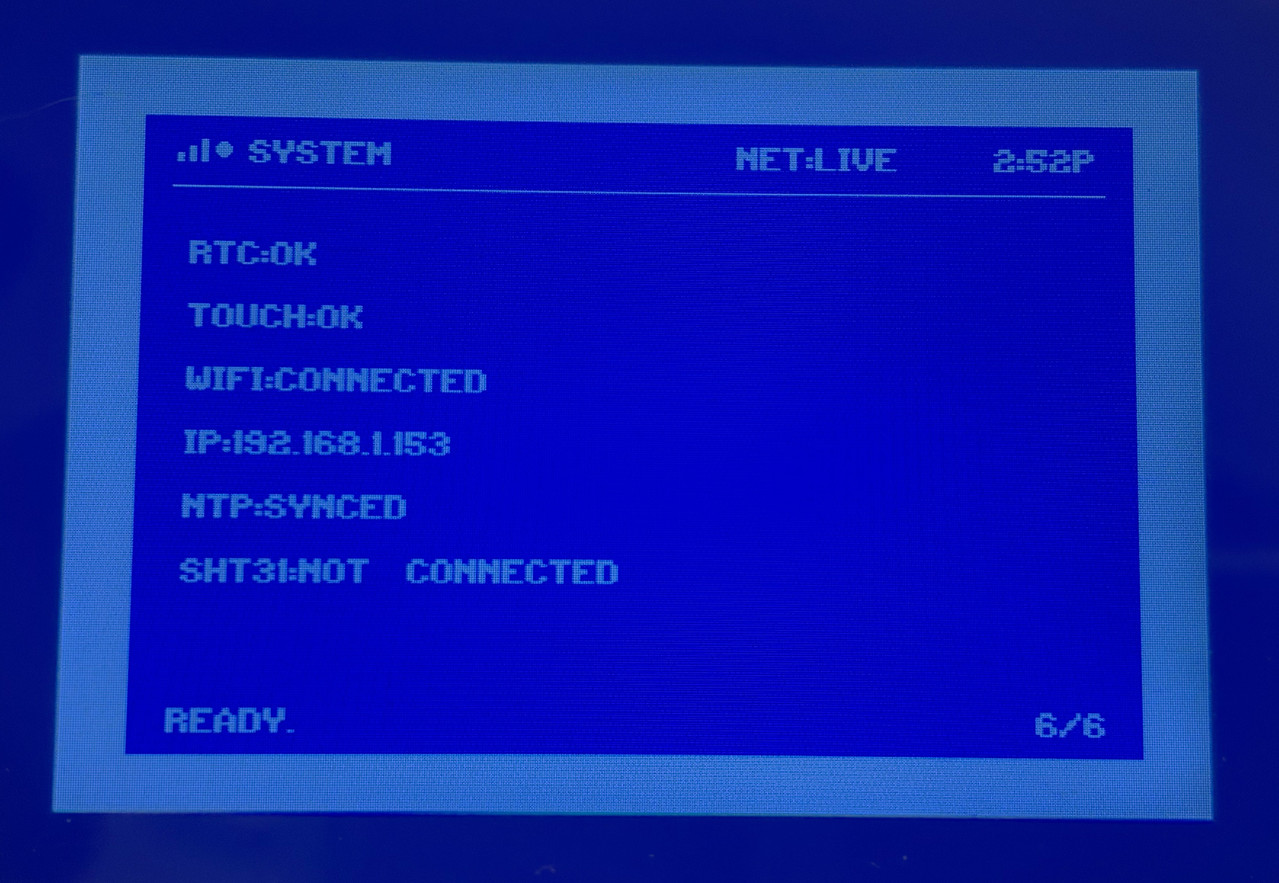

These are more general info type stuff. Clock, some market ETFs, weather forecast, etc. I'm not showing some custom financial calculations I do that tells me specific things about how I invest. The Dividends screen is currently disabled as I incorporated a Developer Mode to cut down on the number of API hits until I get things where I want them.

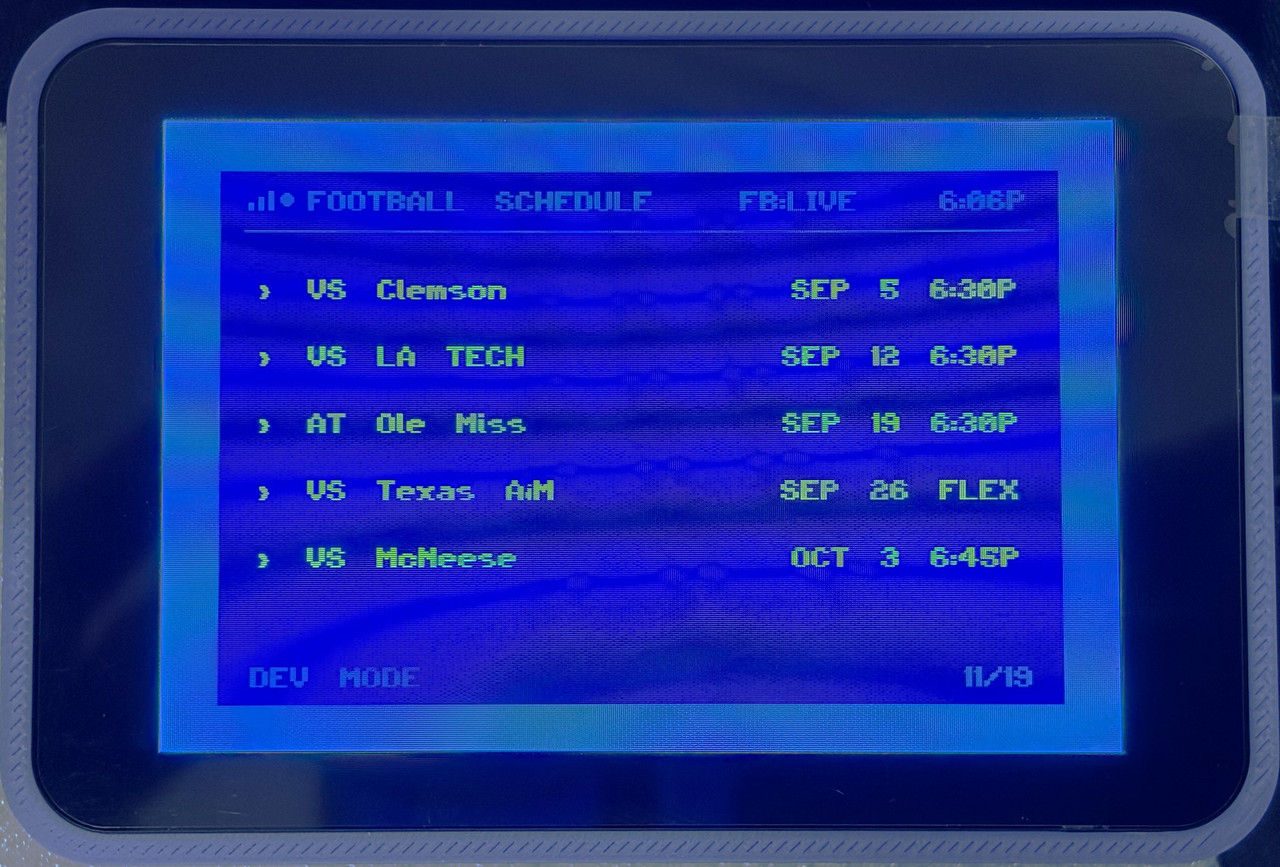

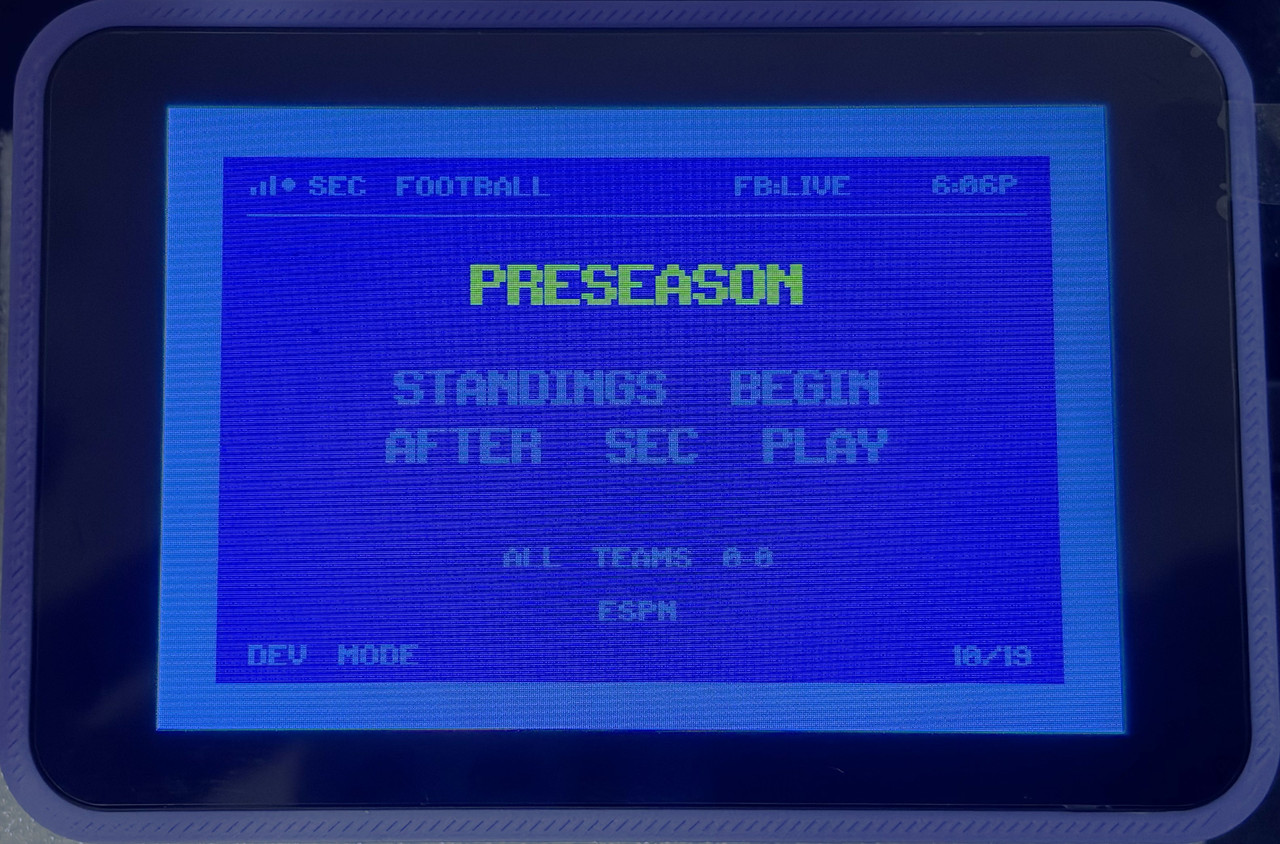

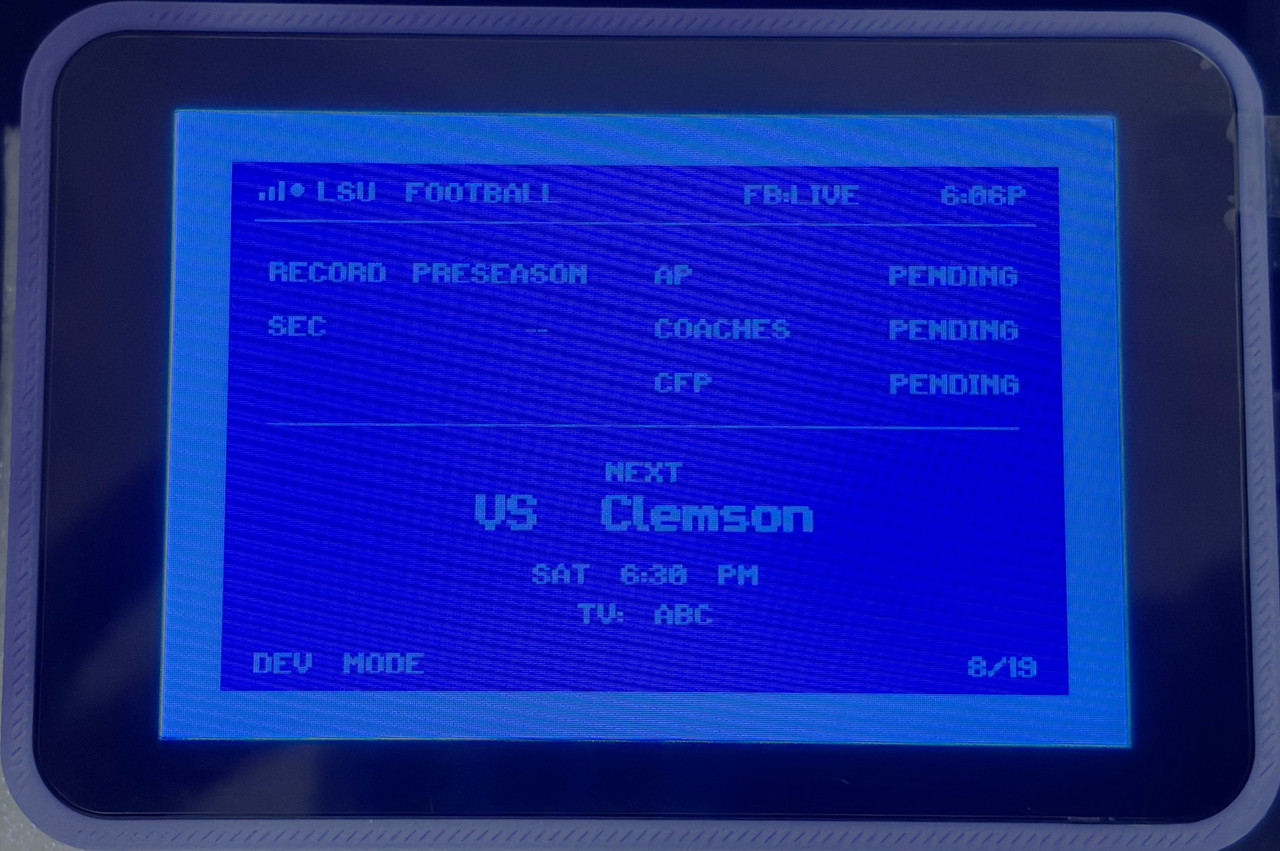

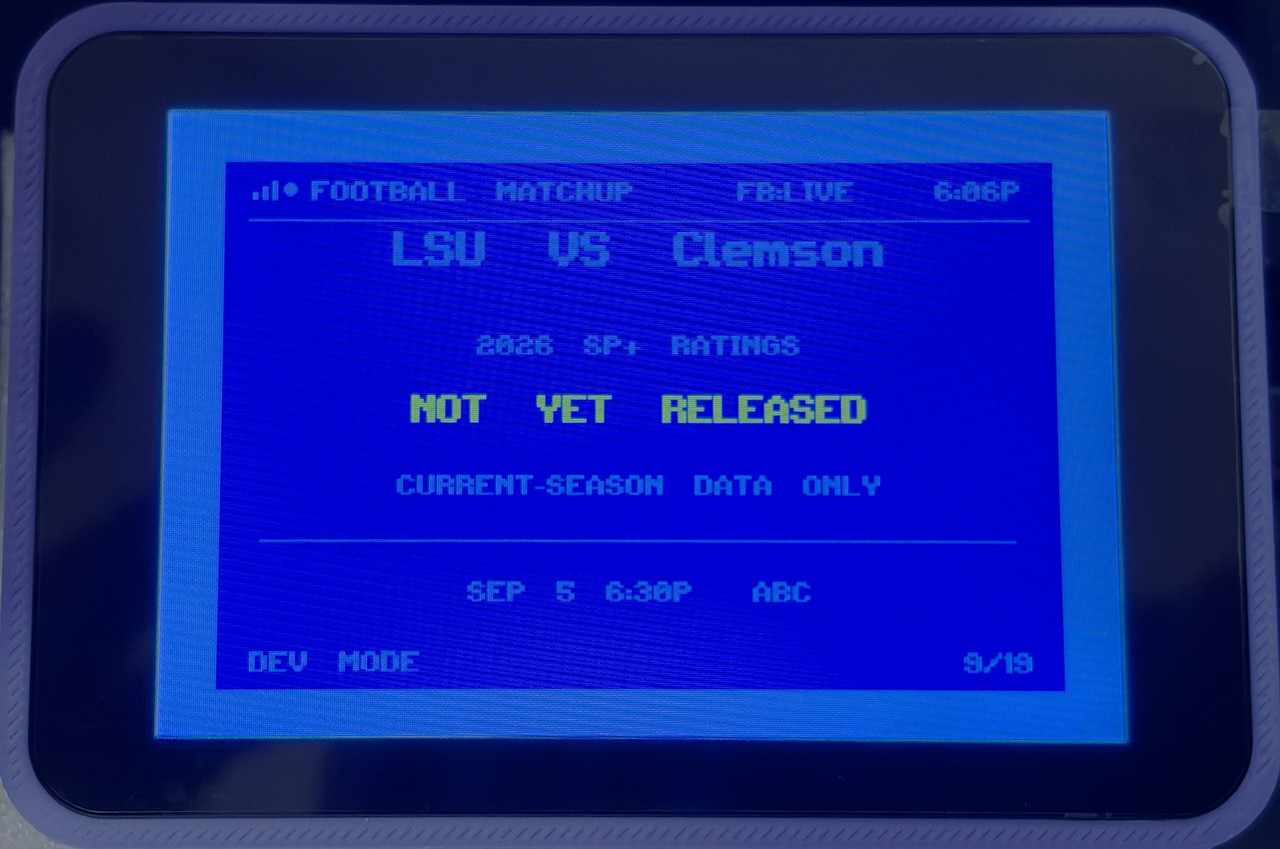

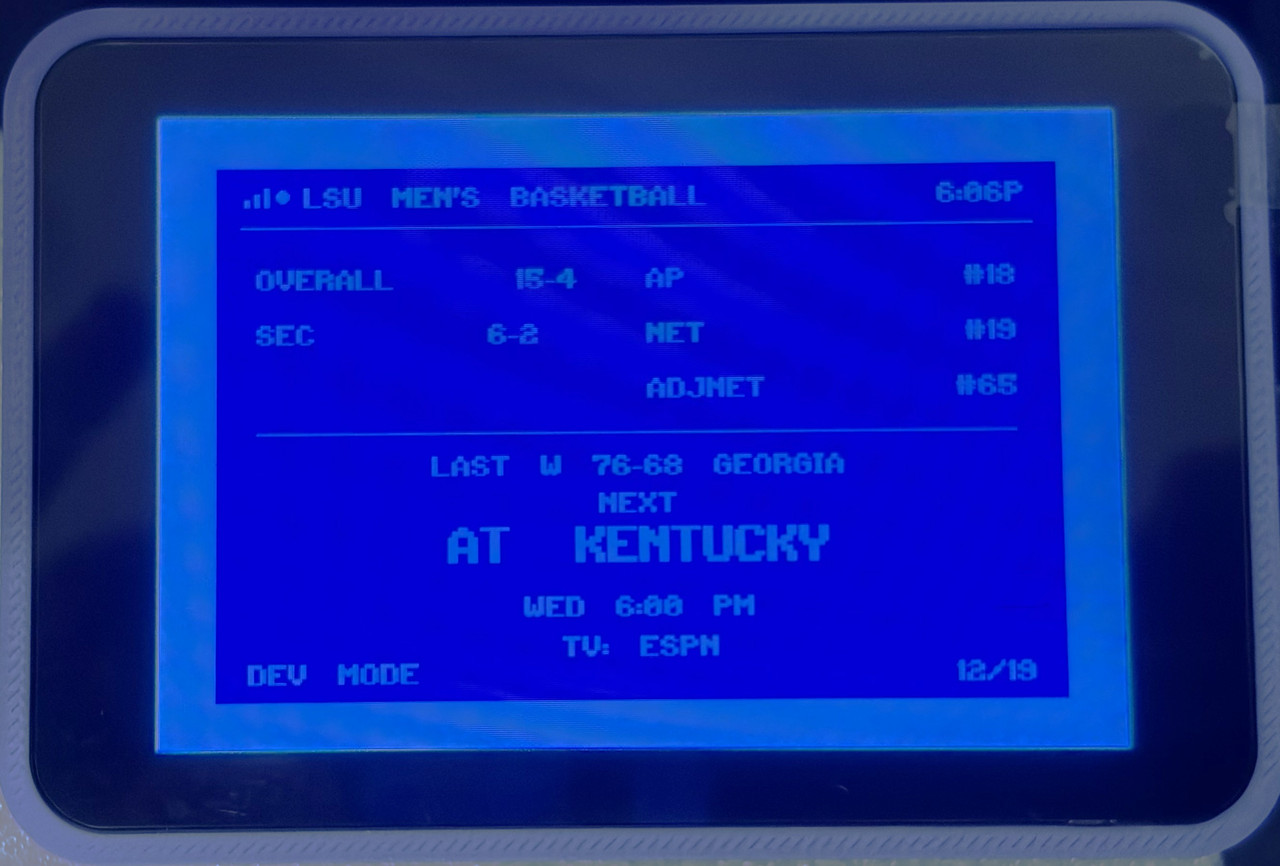

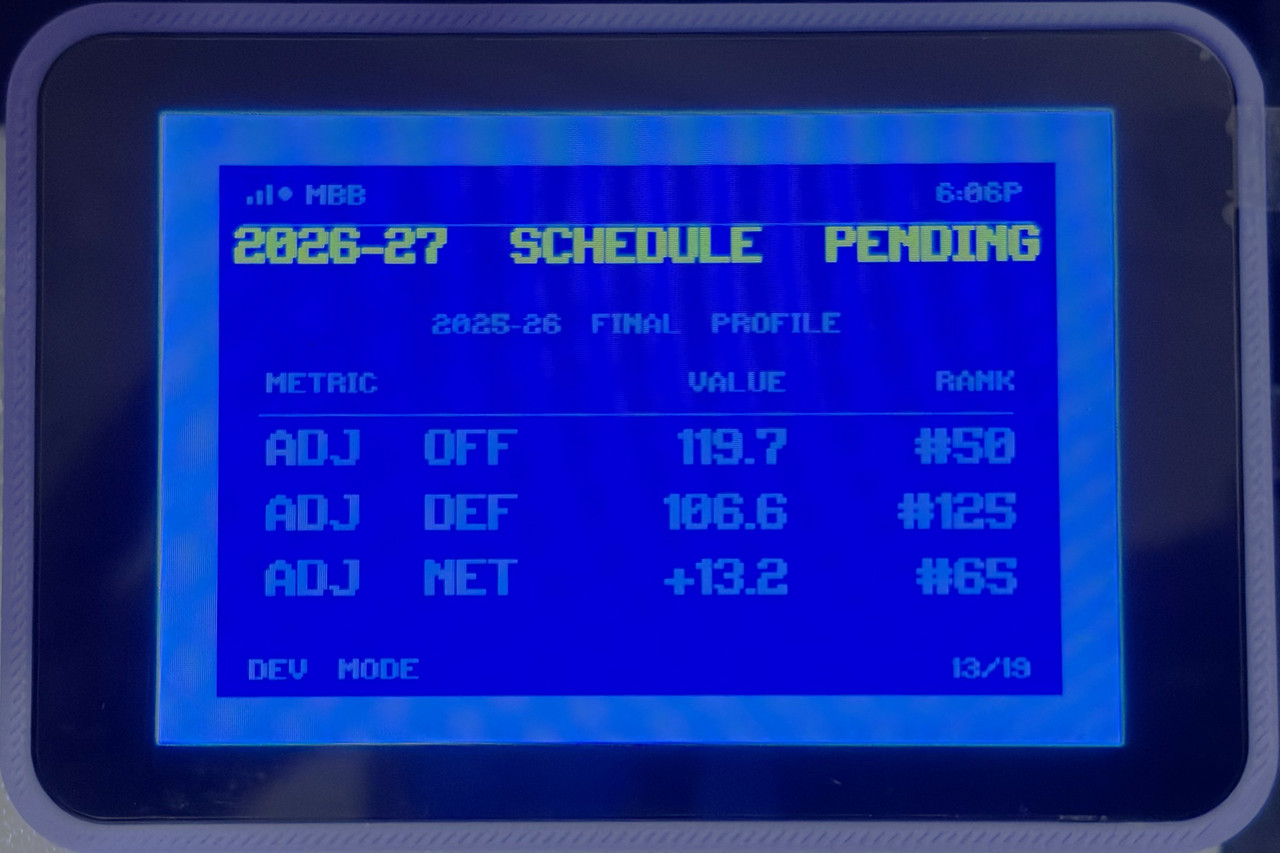

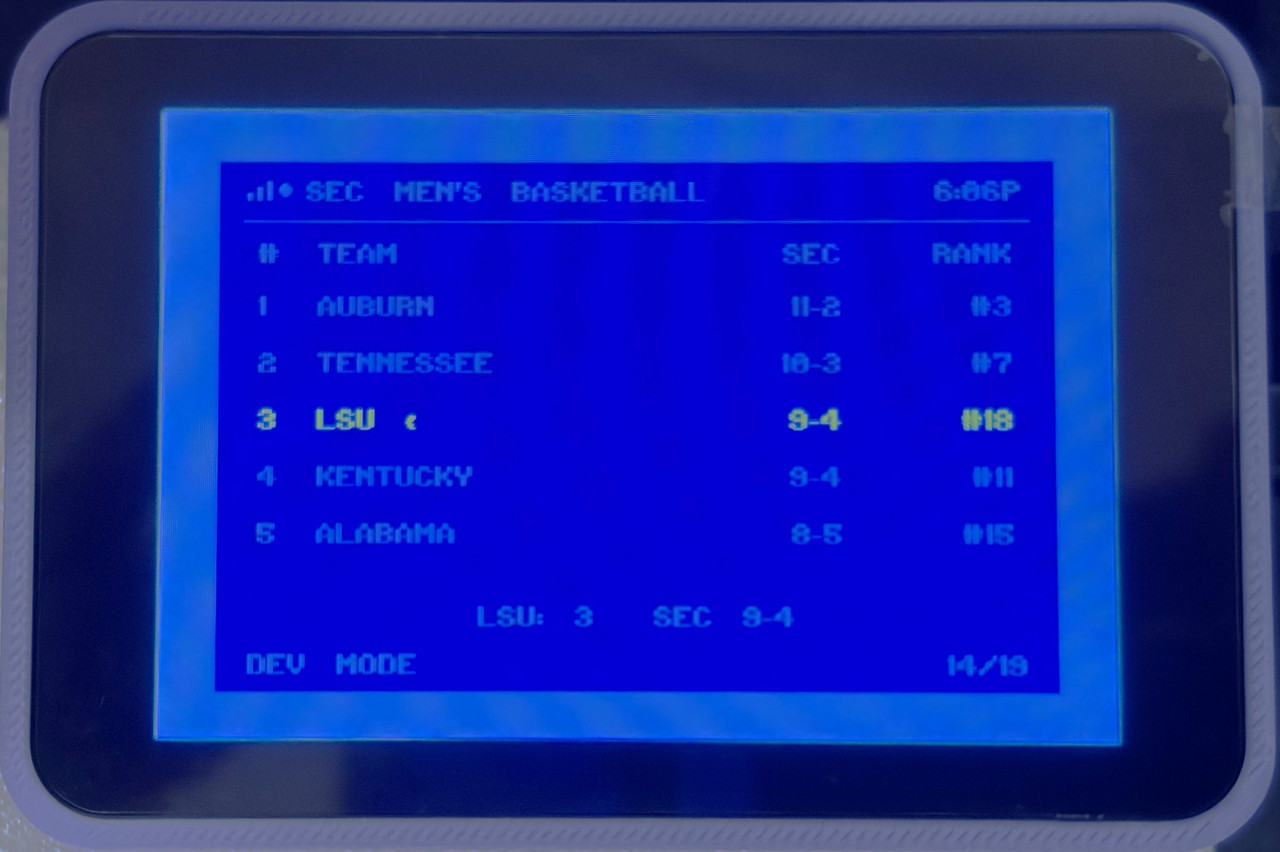

Here's some of the sports screens. The football screens are configured for this season's data (which is why they don't show much). The basketball screens are using both some older data and new as they are still in development. Again, I'm not showing everything.

But you get the idea. I just started with Home Assistant and so I have a lot of other things I can pull in, but I may segregate the HA native stuff and just make the ESP32 for custom use as it's much more versatile for providing information for decision-making, etc. Who knows where I'll end up as I'm just learning about HA and some of the screens in the other HA thread are impressive. This is purposefully retro for now.

This boot sequence is a head nod to Commodore 64 loading a program.

These are more general info type stuff. Clock, some market ETFs, weather forecast, etc. I'm not showing some custom financial calculations I do that tells me specific things about how I invest. The Dividends screen is currently disabled as I incorporated a Developer Mode to cut down on the number of API hits until I get things where I want them.

Here's some of the sports screens. The football screens are configured for this season's data (which is why they don't show much). The basketball screens are using both some older data and new as they are still in development. Again, I'm not showing everything.

But you get the idea. I just started with Home Assistant and so I have a lot of other things I can pull in, but I may segregate the HA native stuff and just make the ESP32 for custom use as it's much more versatile for providing information for decision-making, etc. Who knows where I'll end up as I'm just learning about HA and some of the screens in the other HA thread are impressive. This is purposefully retro for now.

Yep. That’s coming soon. I just installed Home Assistant on my Synology and I’ve got a lot of devices to add. I’m assuming HA can send data via API to the ESP32 and then I’m really off to the races. The real power is customizing everything to meet my specific wants. It’s really cool stuff (for a nerd like me).

I Tried to Build a C64-themed Clock and Failed

Posted by RoyalWe on 7/18/26 at 11:20 pm

I originally bought a 3.5-inch ESP32-S3 touchscreen to build a Commodore 64-style desktop clock -- just for nostalgia.

It now has about 19 screens and is turning into a small C64-themed information terminal.

It currently displays:

* Time, weather and calendar events

* Market, dividend and investment information

* LSU football and basketball schedules, standings, rankings and matchup data

* Wi-Fi and system status

Most of the live information is cleaned up through Google Apps Scripts and sent to the ESP32 as lightweight JSON. LSU football data comes from CollegeFootballData.com, with basketball data coming from CollegeBasketballData.com.

The next step is to move beyond simply displaying data.

I want the device to recognize what matters and provide useful alerts or suggestions. It might warn me that rain is coming before I cut the grass, point out that the HVAC has been running too long without cooling the house, promote an upcoming appointment, or automatically switch to the LSU game screen near kickoff.

I am also evaluating Home Assistant as a backend. It could gather information from my Ecobee thermostats, sensors, NAS, pool equipment and other devices, while the ESP32 remains the custom C64 display and notification system.

I also want to add sound, such as playing an LSU fight-song clip when LSU scores, a C64-style warning for severe weather, or a chime when a 3D print finishes.

The long-term goal is not just a tiny dashboard. I want it to quietly monitor the things I care about, decide what deserves attention and give me useful information when it matters.

I am handling the concept, layouts and testing while using ChatGPT heavily to help write and organize the C++ code.

It has gone well beyond the clock I originally planned, but that has made it a much more interesting project. Who knew ChatGPT could be so useful?

It now has about 19 screens and is turning into a small C64-themed information terminal.

It currently displays:

* Time, weather and calendar events

* Market, dividend and investment information

* LSU football and basketball schedules, standings, rankings and matchup data

* Wi-Fi and system status

Most of the live information is cleaned up through Google Apps Scripts and sent to the ESP32 as lightweight JSON. LSU football data comes from CollegeFootballData.com, with basketball data coming from CollegeBasketballData.com.

The next step is to move beyond simply displaying data.

I want the device to recognize what matters and provide useful alerts or suggestions. It might warn me that rain is coming before I cut the grass, point out that the HVAC has been running too long without cooling the house, promote an upcoming appointment, or automatically switch to the LSU game screen near kickoff.

I am also evaluating Home Assistant as a backend. It could gather information from my Ecobee thermostats, sensors, NAS, pool equipment and other devices, while the ESP32 remains the custom C64 display and notification system.

I also want to add sound, such as playing an LSU fight-song clip when LSU scores, a C64-style warning for severe weather, or a chime when a 3D print finishes.

The long-term goal is not just a tiny dashboard. I want it to quietly monitor the things I care about, decide what deserves attention and give me useful information when it matters.

I am handling the concept, layouts and testing while using ChatGPT heavily to help write and organize the C++ code.

It has gone well beyond the clock I originally planned, but that has made it a much more interesting project. Who knew ChatGPT could be so useful?

re: Who is Your OT Bestie

Posted by RoyalWe on 7/18/26 at 8:59 pm to HoustonChick86

El Gaucho

Iberville...Carondelet...

re: Adding teen to car insurance

Posted by RoyalWe on 7/18/26 at 4:39 pm to KirbySmith

quote:Welcome to the club, buddy.

Just added my 16yo daughter to USAA auto. Went up $600/mo.

re: When do Boomers take ANY accountability?

Posted by RoyalWe on 7/16/26 at 5:24 pm to FATBOY TIGER

quote:Couldn’t agree more. I don’t care what hand you were dealt. Make it happen.

I'm 62 and am accountable for every fricking thing I've done in my life

quote:

liberry

quote:Damn, my grandmother and great grandmother did both of these.

zinc

re: Have you ever used the wrong word?

Posted by RoyalWe on 7/16/26 at 5:16 pm to madamsquirrel

In 7th grade I had to read a section in our biology textbook. Instead of saying “organism” I repeatedly said “orgasm.” The teacher just said afterwards, “I think the word you were looking for was organism.” I took credit for it as my peers high-fived me afterwards.

Who are his handlers? Whose words are he reading?

It’s telling that you’re worried about his reading a thing versus the ideas being communicated, Comrade.

re: When do Boomers take ANY accountability?

Posted by RoyalWe on 7/16/26 at 10:13 am to boogiewoogie1978

This just in: Life’s not fair.

News at 11.

News at 11.

re: “New Orleans thinks they’re so special …” -Gov. Jeff Landry

Posted by RoyalWe on 7/15/26 at 6:35 pm to ErectileReptile

quote:My point was simply that subjective quality-of-life factors can outweigh the financial benefits of staying in a particular place or relationship. I probably buried that point under the colorful language. Different people applying the same principle can still reach different conclusions.

Gotcha, rules for thee but not for me

re: “New Orleans thinks they’re so special …” -Gov. Jeff Landry

Posted by RoyalWe on 7/15/26 at 1:13 pm to ErectileReptile

Of course you could. I wouldn’t, but you’re welcome to do so.

re: “New Orleans thinks they’re so special …” -Gov. Jeff Landry

Posted by RoyalWe on 7/15/26 at 11:55 am to ErectileReptile

quote:With my accruing wisdom, I've discovered that feelings have a legitimate place in a lot of decisions we make that many believe shouldn't. Whether you call it personal taste or expected utility, sometimes the "irrational" decision is the right one for quality of life or some other subjective reason. For that reason, frick New Orleans, its shitty attitude, its shitty politicians, its criminals, its potholes, and its populace.

Facts over feelings though right

re: NJ woman, 25, charged with sexually assaulting young boy

Posted by RoyalWe on 7/14/26 at 12:54 pm to Darth_Vader

This is the first time what I thought was going to be a "not guilty" verdict quickly became "guilty" and get a rope. Sick individual.

Popular