Started By

Message

re: OT- Cooking the Books

Posted on 8/9/16 at 8:23 pm to deeprig9

Posted on 8/9/16 at 8:23 pm to deeprig9

??

The guy who claims he has his 7, that's recommending folks buy CEF's inside a ROTH while we're all teetering on the edge of a fiscal cliff, is now quoting Ben Affleck in lines from Boiler Room.

Yes, let's shame people for not chasing winners while the market's at all time highs and overdue for a correction. And why not badger folks for being conservative and cautious and tell them financial advisors are all blood sucking fee vampires too. Everyone should be capable of making huge gains at all times in every market all by themselves.

Dude, just shut your pie hole and stop acting like something you're clearly not. After hearing your "advice" and "investing prowess", I'd bet dollars to donuts you're full of horse shite and in the lower half of middle classdom barely scraping by and trading on old 401k rollovers from jobs you were fired from.

The guy who claims he has his 7, that's recommending folks buy CEF's inside a ROTH while we're all teetering on the edge of a fiscal cliff, is now quoting Ben Affleck in lines from Boiler Room.

Yes, let's shame people for not chasing winners while the market's at all time highs and overdue for a correction. And why not badger folks for being conservative and cautious and tell them financial advisors are all blood sucking fee vampires too. Everyone should be capable of making huge gains at all times in every market all by themselves.

Dude, just shut your pie hole and stop acting like something you're clearly not. After hearing your "advice" and "investing prowess", I'd bet dollars to donuts you're full of horse shite and in the lower half of middle classdom barely scraping by and trading on old 401k rollovers from jobs you were fired from.

3

3

Posted on 8/9/16 at 8:38 pm to BeefDawg

U so mad bro

Posted on 8/9/16 at 8:55 pm to BeefDawg

quote:

in the lower half of middle classdom barely scraping by and trading on old 401k rollovers from jobs you were fired from.

That's a financial planner mike drop right there.

Posted on 8/10/16 at 8:08 am to deeprig9

I always take the distribution.

It's never up to the broker.

Investments and what to do with them should be your choice, not the broker's.

I'm sure they offer a reinvestment option.

It's never up to the broker.

Investments and what to do with them should be your choice, not the broker's.

I'm sure they offer a reinvestment option.

Posted on 8/10/16 at 8:23 am to samson'sseed

quote:

I'm sure they offer a reinvestment option.

DRIPs

Posted on 8/15/16 at 11:41 am to BeefDawg

I spent this morning reading up on CEF's in Roth's and it turns out they are the absolute best place to hold such assets with 1 exception...

If you are heavily invested in income funds overall, you are better off to have your straight-up dividend yeilding funds in your Roth and the CEF somewhere not tax protected, because of the already inherent tax advantage of ROC.

And depending on your tax status right now, you may be even better off with a CEF in a plain old individual brokerage account to get the immediate tax benefit, and not worrying about the future tax consequenses (like if you are already retired and living off the income day to day).

If you are heavily invested in income funds overall, you are better off to have your straight-up dividend yeilding funds in your Roth and the CEF somewhere not tax protected, because of the already inherent tax advantage of ROC.

And depending on your tax status right now, you may be even better off with a CEF in a plain old individual brokerage account to get the immediate tax benefit, and not worrying about the future tax consequenses (like if you are already retired and living off the income day to day).

Posted on 8/17/16 at 9:24 am to deeprig9

In 9 days I'm up 4.5% and the S&P is down .5%

Thanks for this one, Squatch!

Thanks for this one, Squatch!

Posted on 8/18/16 at 7:57 am to deeprig9

Toilet paper...never going to go out of style and there are more assholes born than die every year....everything else in life is a fad but shitting never ends....

Posted on 8/18/16 at 8:11 am to deeprig9

Short term means nothing, unless you are a day trader.

I have some advice for when you are interested in purchasing a stock or fund.

I noticed you purchased those shares of IRR immediately.

You should never pay the market price for a stock because between the time you order and the order goes through the price can freakishly spike, then decline. You can end up paying too much.

Instead, you should make a limit order. Study the price history of the stock, then order it at a limit price. Select the average lower price for the stock that it often falls to. Then be patient and wait.

Chances are you will always get the stock or fund at a lower price. The stock market always fluctuates and you can almost surely count on purchasing those shares for cheaper, especially after a bad day, week, or month.

I have some advice for when you are interested in purchasing a stock or fund.

I noticed you purchased those shares of IRR immediately.

You should never pay the market price for a stock because between the time you order and the order goes through the price can freakishly spike, then decline. You can end up paying too much.

Instead, you should make a limit order. Study the price history of the stock, then order it at a limit price. Select the average lower price for the stock that it often falls to. Then be patient and wait.

Chances are you will always get the stock or fund at a lower price. The stock market always fluctuates and you can almost surely count on purchasing those shares for cheaper, especially after a bad day, week, or month.

Posted on 8/30/16 at 9:19 am to samson'sseed

Limit orders cost me more.

IRR still WINNING

IRR still WINNING

Posted on 8/30/16 at 9:40 am to deeprig9

The Fed is talking about raising interest rates.

I suggest buying stock in some anal lubricant.

I suggest buying stock in some anal lubricant.

Posted on 8/30/16 at 10:52 am to BeefDawg

Impending rate hike is already built into today's equity. Not worried.

Posted on 8/30/16 at 12:24 pm to deeprig9

Some of the advice here is scary... to be fair, your investment goals and risk tolerance are not nearly clear enough for anyone to be giving blanket investment advice without major caveats.

That being said, sound like you may like a solid low fee diversified dividend etf? (SDY for example) not sure why you want to be weighted more heavily towards REIT exposure exactly but there are plenty of good REIT ETFs with low expense ratios as well (VNQ).

Also the debate on whether "cash is king" totally depends on your liquidity needs and your current progress with maxing out your tax-advantages accounts. Roth IRA principal can be pulled quickly and penalty free anytime though.

Check out something like bogleheads.com forum for actual advice, I'm sure variations on your question has been asked and discussed much more rigorously on there multiple times.

That being said, sound like you may like a solid low fee diversified dividend etf? (SDY for example) not sure why you want to be weighted more heavily towards REIT exposure exactly but there are plenty of good REIT ETFs with low expense ratios as well (VNQ).

Also the debate on whether "cash is king" totally depends on your liquidity needs and your current progress with maxing out your tax-advantages accounts. Roth IRA principal can be pulled quickly and penalty free anytime though.

Check out something like bogleheads.com forum for actual advice, I'm sure variations on your question has been asked and discussed much more rigorously on there multiple times.

Posted on 8/30/16 at 1:56 pm to deeprig9

quote:

Impending rate hike is already built into today's equity.

Umm, IRR is a Natural Resources fund.

Apple, Google, Verizon, and Microsoft have excess capital sitting around in case of rate hikes. Natural resource small-cap companies inside a fund trading at $6/share do not.

Posted on 8/30/16 at 5:53 pm to deeprig9

Then you should use Scottrade or some other similar brokerage.

Scottrade charges $7 a trade.

Most brokerages don't charge extra for limit orders.

Scottrade charges $7 a trade.

Most brokerages don't charge extra for limit orders.

Posted on 8/30/16 at 5:59 pm to BeefDawg

Yeah, when the Fed raises interest rates, stocks may fall for a few days, but they will rally soon after.

Even if they raise rates, the average dividend payout is still a far better investment than keeping money in the bank.

Now, if certificates of deposit increase to 3%, I will start reducing my exposure to the stock market.

BTW, I am already accumulating cash from dividends in anticipation of this happening. I am not reinvesting what I have accumulated until the stock market tanks big time again. I am waiting for a major correction. I am in an holding pattern.

Even if they raise rates, the average dividend payout is still a far better investment than keeping money in the bank.

Now, if certificates of deposit increase to 3%, I will start reducing my exposure to the stock market.

BTW, I am already accumulating cash from dividends in anticipation of this happening. I am not reinvesting what I have accumulated until the stock market tanks big time again. I am waiting for a major correction. I am in an holding pattern.

This post was edited on 8/30/16 at 6:00 pm

Posted on 8/30/16 at 11:13 pm to samson'sseed

Have you ever heard of Kondratieff Economic Wave Cycles?

If not, do some research on them. Kondratieff was a Russian economist back in 1925 who found a wave-like pattern going back to the late 1700's and when applied from then to now, it has proven almost perfectly accurate in predicting global economic events.

K-Wave cycle theory has us in an almost identical trajectory to the 1928-29 global economic crash that kicked off our Great Depression in 1929.

Right now, Europe is on the verge of economic collapse. The EU will break up any day now, and with it will crumble the Euro. Japan has just had its 4th straight quarter of recession, which means they are now in a depression by definition. Japan and China will start going at each other before too long over land and resources they both claim they own.

The same thing happened in the late 1920's. Half the countries of Europe and Asia had financial meltdowns and crashed.

When this happened, the US markets also dropped and completely crashed once global trade came to a screeching halt. And then something peculiar happened. Every rich and super wealthy bloke in Europe and Asia made their way to the US and began investing in our markets because the Dollar was still strong due to the gold standard still backing it. And our stock market went from 47 in 1932 to 197 by 1937. A 313% gain in just 5 years.

Well this is the same thing that's going to happen here except faster.

Europe and Japan are going to crash. Our markets are going to panick and have massive sell offs and a mini-crash. But then every rich clown in Europe and Asia is going to unload their wealth in our market in companies that have been stockpiling cash reserves, and our market is going to skyrocket up for about a year or so. Like maybe even hit 25,000 to 30,000.

But then it's all going to catch up to us. The debt, the under-funded liabilities, the wasteful over-spending combined with global trade being crushed, and us sitting in an inflation/currency/interest rate bubble that has hit its limits and bursts. And within 6-12 months, our markets will be below 10,000, and possibly as low as 6,000 again.

It's going to get crazy soon. If you don't maneuver through this incoming wave properly, you can lose your arse bad. But if you get out and back in and then back out at just the right times and invested in the right things, you can be set for life.

If not, do some research on them. Kondratieff was a Russian economist back in 1925 who found a wave-like pattern going back to the late 1700's and when applied from then to now, it has proven almost perfectly accurate in predicting global economic events.

K-Wave cycle theory has us in an almost identical trajectory to the 1928-29 global economic crash that kicked off our Great Depression in 1929.

Right now, Europe is on the verge of economic collapse. The EU will break up any day now, and with it will crumble the Euro. Japan has just had its 4th straight quarter of recession, which means they are now in a depression by definition. Japan and China will start going at each other before too long over land and resources they both claim they own.

The same thing happened in the late 1920's. Half the countries of Europe and Asia had financial meltdowns and crashed.

When this happened, the US markets also dropped and completely crashed once global trade came to a screeching halt. And then something peculiar happened. Every rich and super wealthy bloke in Europe and Asia made their way to the US and began investing in our markets because the Dollar was still strong due to the gold standard still backing it. And our stock market went from 47 in 1932 to 197 by 1937. A 313% gain in just 5 years.

Well this is the same thing that's going to happen here except faster.

Europe and Japan are going to crash. Our markets are going to panick and have massive sell offs and a mini-crash. But then every rich clown in Europe and Asia is going to unload their wealth in our market in companies that have been stockpiling cash reserves, and our market is going to skyrocket up for about a year or so. Like maybe even hit 25,000 to 30,000.

But then it's all going to catch up to us. The debt, the under-funded liabilities, the wasteful over-spending combined with global trade being crushed, and us sitting in an inflation/currency/interest rate bubble that has hit its limits and bursts. And within 6-12 months, our markets will be below 10,000, and possibly as low as 6,000 again.

It's going to get crazy soon. If you don't maneuver through this incoming wave properly, you can lose your arse bad. But if you get out and back in and then back out at just the right times and invested in the right things, you can be set for life.

Posted on 8/31/16 at 9:15 am to BeefDawg

Sorry, but Europe is not anywhere close to an economic collapse.

The EU will not break up.

I don't know where you get this doomsday crap.

The EU will not break up.

I don't know where you get this doomsday crap.

Posted on 8/31/16 at 10:27 am to samson'sseed

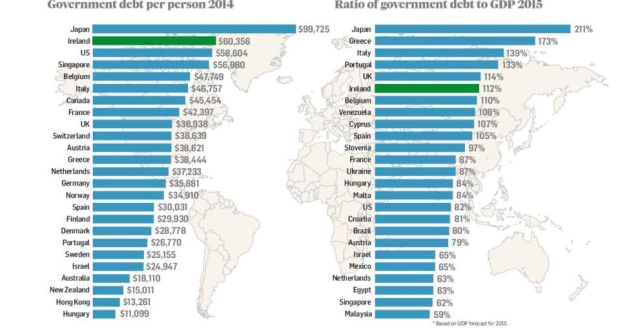

Of the 28 countries in the EU, at least 19 of them are in unsustainable debt accumulation and 25 of them are deficit spending (spending more than their tax revenue). And 10 of them are even spending annually more than their entire country's annual GDP, while the remaining 15 are deficit spending between 15%-50% above their tax revenue.

Spain tax payers, for instance, would have to pay 100% tax just to nearly break even with their government's annual spending.

These countries are deficit spending and their debt is skyrocketing at rates that can't possibly be sustained.

Banks in Europe are at NEGATIVE interest rates, meaning it actually costs the consumer money just to store their earnings in a bank.

The Euro was $1.59 in 2008, it's now at $1.11 and this is after we have DOUBLED our M2 money supply from $6 trillion to $12 trillion of currency in circulation. How the hell does the Euro go down when we should essentially have inflated the Dollar by 100%?

And the refugee crisis is going to push these countries over the cliff. A bunch of foreign speaking immigrants who aren't working because of a language, education, and labor skill barrier, but are now siphoning gobs of welfare benefits out of the tax coffers, is going to bowl through their economies.

Japan is in even worse shape than Greece as far as debt is concerned. The only saving grace they have is a strong manufacturing and export industry. But they supplant that with selling goods at lower costs than everyone else. But they can't keep that up. They're losing too much money and going too far in debt.

So go ahead and invest in EU and Japanese emerging markets. I dare ya.

Spain tax payers, for instance, would have to pay 100% tax just to nearly break even with their government's annual spending.

These countries are deficit spending and their debt is skyrocketing at rates that can't possibly be sustained.

Banks in Europe are at NEGATIVE interest rates, meaning it actually costs the consumer money just to store their earnings in a bank.

The Euro was $1.59 in 2008, it's now at $1.11 and this is after we have DOUBLED our M2 money supply from $6 trillion to $12 trillion of currency in circulation. How the hell does the Euro go down when we should essentially have inflated the Dollar by 100%?

And the refugee crisis is going to push these countries over the cliff. A bunch of foreign speaking immigrants who aren't working because of a language, education, and labor skill barrier, but are now siphoning gobs of welfare benefits out of the tax coffers, is going to bowl through their economies.

Japan is in even worse shape than Greece as far as debt is concerned. The only saving grace they have is a strong manufacturing and export industry. But they supplant that with selling goods at lower costs than everyone else. But they can't keep that up. They're losing too much money and going too far in debt.

So go ahead and invest in EU and Japanese emerging markets. I dare ya.

This post was edited on 8/31/16 at 10:29 am

Posted on 8/31/16 at 8:30 pm to BeefDawg

In a global meltdown as you've described, wouldnt an annuity/whole life return also be worthless? Arent those also predicated on equity markets behind the curtain?

Page 5 of 6

Page 5 of 6

Latest Georgia News

Popular

Back to top